On this page

How the modern debit card helps billers deliver seamless payment experiences

Debit cards have a branding problem. They’re often dismissed as legacy plastic: simple, utilitarian, and static. But debit is one of the most powerful connective tissues in modern payments. It’s the silent engine behind mobile wallets, network tokenization, biometric checkout, and the next generation of always-on, API-driven payment experiences. And consumers are already treating debit this way: according to independent research from Javelin Strategy, data shows that most shoppers now use debit cards to fund mobile wallets like Apple Pay, Google Pay, Samsung Pay, PayPal, Venmo, and Cash App, which is clear evidence that debit is no longer “old tech,” but the default credential shaping digital commerce.

Cards continue to play a central role in bill pay and recurring payments, giving customers a familiar, trusted way to complete transactions across channels. For billers, debit is often the credential behind those “just works” moments—delivering the reliability, cost efficiency, and continuity needed to keep payment volumes moving without interruption. And as billers face mounting pressure to reduce declines, expand payment choice, simplify digital journeys, and control acceptance costs, modern debit is emerging as a far more strategic asset than its reputation suggests.

The hidden infrastructure behind modern payment UX

Why debit sits beneath today’s mobile‑first experiences

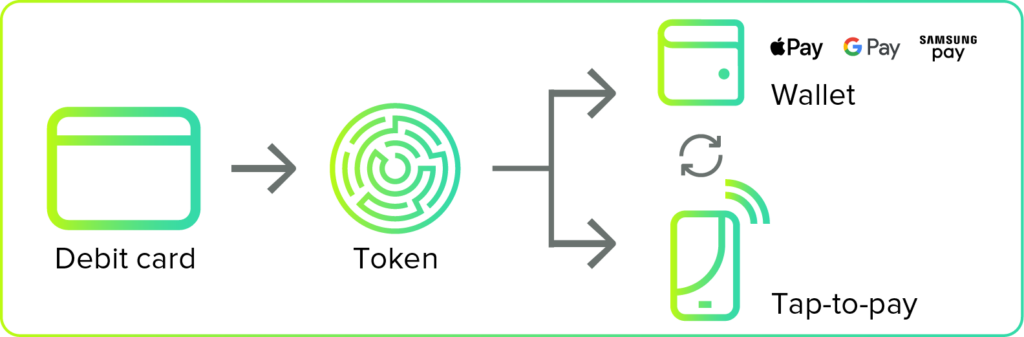

Debit has become the default credential inside mobile wallets because it’s the payment method consumers trust most, the one they use every day, and the one with immediate funds availability. Its ubiquity across banks and devices means it works anywhere a wallet works, giving both consumers and networks a reliable, ready‑to‑use foundation. This reliability is exactly why debit consistently emerges as the credential powering alternative payments such as digital wallets and other mobile‑first experiences.

When consumers tap their phones at checkout or autofill payment details in an app, they’re not thinking about the credential beneath it. But the credential most often powering that experience is a debit card. Debit credentials sit at the center of the modern payments ecosystem, enabling:

- Apple Pay

- Google Pay

- Samsung Pay

- Network tokens used across digital commerce

This means debit isn’t just compatible with today’s digital experiences, it’s foundational. Mobile wallets and tokenization layers are only as strong and seamless as the payments instrument underneath them. Independent analysis from The Paypers confirms this, noting that wallets such as Apple Pay, Samsung Pay, and Google Pay are usually card‑backed, most commonly by a debit card, making debit the underlying credential driving today’s mobile‑first, tokenized payment experiences. Debit is that instrument.

Network tokenization: From “card on file” to intelligent, always-fresh credentials

Network tokenization is transforming payments reliability, especially in recurring or stored card scenarios.

According to industry analyses, network tokenization significantly reduces declines caused by outdated or unavailable card credentials, as tokens automatically update in the background when a card is replaced or reissued. This keeps user accounts always up to date, reducing checkout friction and preventing unnecessary interruptions.

That means:

- Fewer false declines

- Improved authorization rates

- Lower customer frustration

- Less operational overhead tied to credential lifecycle management

It’s the type of infrastructural modernization that consumers never see—but immediately feel.

Wallet-based debit: Where convenience meets conversion

When debit becomes a wallet-based token rather than physical plastic, it unlocks a cascade of UX improvements:

- Biometric authentication: Face ID, fingerprint, device-level security, all layered before the token ever reaches the merchant

- Faster checkout: One tap. No manual entry. No mistyped numbers. Higher trust. Lower friction

- Higher conversion rates: When authentication is effortless, and payment credentials are always up to date, abandonment drops, and revenue goes up

Consumers feel like the experience “just works.” Merchants make more successful transactions. Issuers reduce operational pain. Everyone wins, even if no one sees the debit credential quietly doing the work. And that’s the real power of wallet-based debit: it disappears into the background while elevating every part of the payments journey. It’s the silent engine that keeps mobile pay moving securely, instantly, and reliably, proving that the most transformative technologies are often the ones you never notice.

Debit as an API-based value object

As digital payments continue to evolve, the very idea of what a “debit card” is, and what it can do, is being redefined. What once lived as a static piece of plastic in a wallet is now becoming a dynamic, intelligent, software-driven asset that moves fluidly through the modern payments stack. Debit is no longer limited to magnetic stripes and card readers; it now lives in APIs, wallets, encrypted tokens, and device-level identity frameworks. This shift marks a fundamental transformation: debit isn’t just participating in the digital payments ecosystem—it’s becoming one of its most versatile and programmable building blocks.

The biggest shift underway is conceptual, not technical: Debit is evolving from a static card into a dynamic, API-addressable value object. Instead of being defined by 16 digits embossed on plastic, debit credentials are now:

- Tokenized, format flexible, lifecycle-managed instruments

- Portable across apps, devices, rails, and channels

- Interpreted by networks and wallets, not just card readers

- Integrated with risk engines, behavioral models, and fraud intelligence

This positions debit as a programmable payment primitive, something that can be orchestrated, optimized, and enriched far beyond its original design.

Why this matters for billers

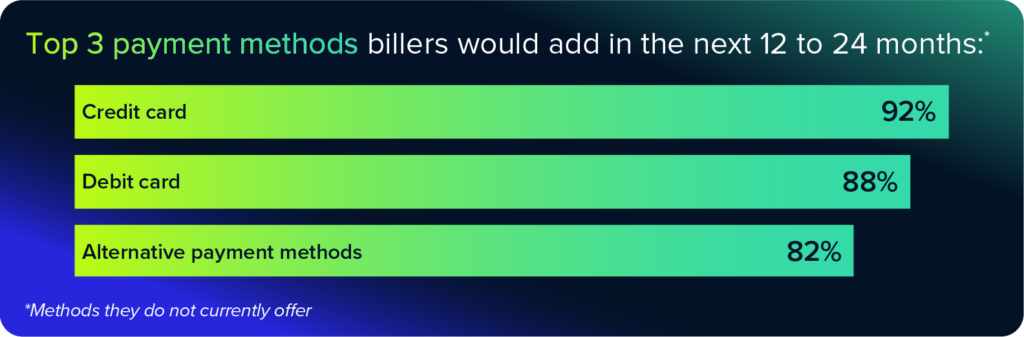

The shift toward digital-first payments isn’t slowing. In fact, billers are already moving in this direction. According to the 2026 ACI Speedpay Biller Impact Study, debit is one of the top payment methods billers plan to expand over the next 12–24 months, as they prioritize lower‑cost payment options and more reliable digital experiences. Debit cards’ ability to reduce fees, lower decline rates, and seamlessly support mobile‑first, tokenized payment flows aligns directly with billers’ goals of cutting operational friction and meeting rising consumer expectations.

Younger consumers are also helping pull debit into the mainstream. Findings from the 2026 ACI/YouGov Income Tax Payment Trends Report show that, while every generation would choose debit to avoid higher transaction fees, younger generations are especially likely to do so. 71% of Gen X, 65% of Millennials, and 68% of Gen Z say they would switch to debit when credit fees rise. Gen Z in particular leads all generations in actual debit usage for paying taxes owed, with 25.24% choosing debit, making it their top card-based payment method. This shift highlights that debit isn’t just a legacy card—it’s the preferred, cost-efficient choice for digital-native consumers during high stakes, fee-sensitive moments. For billers, this reinforces debit’s growing relevance as a payment method that aligns with both consumer behavior and modern digital expectations.

Debit: The quiet catalyst of always-on payments

“Old plastic” was never the whole story. Debit has become:

- The credential behind mobile wallets, serving as the primary funding source for Apple Pay, Samsung Pay, Google Pay, PayPal, Venmo, and Cash App—wallets that increasingly dominate digital checkout experiences.

- The foundation of network tokenization, where debit credentials are transformed into lifecycle-managed, continuously refreshed network tokens that reduce declines, strengthen security, and stabilize authorization rates.

- The engine driving faster, safer, biometric-authenticated checkout, enabling tap-to-pay flows that combine device-level identity, tokenized credentials, and instant authorization.

- The payments object fueling API-driven innovation, where debit credentials now operate as dynamic, programmable value objects that integrate seamlessly across gateways, orchestration layers, fraud platforms, and mobile-first commerce.

As billers, providers, and platforms push toward frictionless, always‑available payments, debit is no longer something to overlook. It’s something to build on. Debit’s ubiquity, stability, and deep integration across wallet ecosystems make it one of the most future-proof instruments in modern payments—especially as digital wallets accelerate globally and increasingly rely on card-backed credentials rather than stored balances or bank transfers.

Because when systems fail, tokens refresh, cards get reissued, or devices change… debit keeps payments moving. It’s the credential that persists beneath every tap, token, and wallet, a dependable anchor in a rapidly shifting payments landscape. And that’s exactly why ACI Speedpay’s vision is built around one simple promise: never miss a payment. Debit makes that possible.

And as billers navigate growing consumer expectations, rising cost pressures, and the shift toward mobile‑first, tokenized experiences, debit’s role will only continue to strengthen. Even as billers offer more ways to pay, the debit card remains a dependable, cost‑efficient choice that fits naturally into mobile‑first, tokenized payment flows.

For a deeper look at the trends shaping these choices, explore the 2026 ACI Speedpay Biller Impact Study.

Why are debit cards becoming more important for billers?

Debit helps billers balance what matters most in digital bill pay: cost, continuity, and customer experience. As more customers store debit in mobile wallets and use it for everyday payments, debit is becoming a practical way to reduce friction, support digital-first journeys, and keep payments flowing reliably across channels.

How does debit improve authorization rates and reduce declines?

Debit performance improves when billers use network tokenization and credential lifecycle updates. Tokenized credentials can stay current when cards are reissued or replaced, which helps reduce declines caused by outdated card-on-file data and supports more consistent authorization success in recurring and wallet-based transactions.

What makes debit well-suited for mobile-first and wallet-based payments?

Debit is widely issued and familiar, which makes it easy for customers to adopt in wallets. In wallet-based flows, tokenization and device-based authentication (like biometrics) can add security while enabling faster, lower-effort checkout and bill pay experiences—often turning payment into a true one-tap moment.

Are younger consumers really driving the shift toward debit?

In many cases, yes. Younger segments often use debit for day-to-day spending and wallet-based payments, especially when they want predictability and control. That behavior supports billers’ priorities around lower-cost acceptance, payments certainty, and mobile-first engagement.

Does debit replace other payment methods?

No. Debit complements credit, ACH, real-time payments, and other options. Most billers still need a mix to match customer preferences—debit is simply becoming a more central credential as payments shift toward tokenized, mobile-first experiences.

Pierce English Sr. is a New Business Developer at ACI Speedpay, where he partners with financial institutions and billers to modernize digital payment experiences. With deep expertise in consumer payments and bill pay strategy, Pierce helps organizations deliver faster, more intuitive, and mobile-first payment experiences for consumers. His work centers on technologies quietly shaping the future of payments, particularly how debit underpins mobile wallets, tokenization, and faster pay experiences. Pierce brings a clear perspective on how debit enables secure, low-friction transactions behind the scenes, supporting seamless wallet adoption, trusted tokenized credentials, and the speed today’s consumers expect. Known for translating complex payment innovation into practical business value, Pierce regularly shares insights on digital adoption, mobile payments, and evolving consumer expectations. His approach bridges strategy and execution, helping organizations stay ahead as payments continue to become faster, simpler, and more embedded in everyday experiences.