On this page

The risk of not offering debit to your customers

When debit isn’t offered (or isn’t easy to find and use), customers who prefer it are forced into higher-friction paths: switching rails, re-entering bank details, abandoning self-serve and calling an agent, or delaying payment until they can use their preferred method. That creates measurable downstream cost for billers: more failed attempts, more exceptions to research and resolve, higher contact-center volume, and less predictable cash flow. In an always-on bill-pay environment, debit needs to be treated as a first-class option, not a fallback.

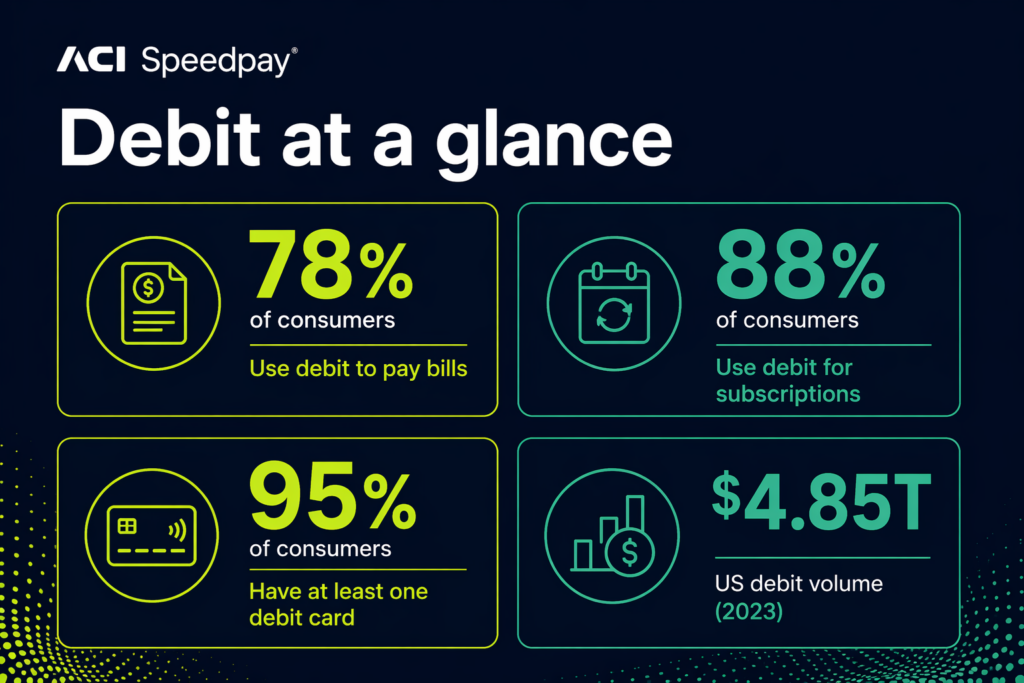

For years, debit has carried an unfair reputation as “simple plastic,” a basic, utilitarian payment method overshadowed by credit cards, digital wallets, and emerging fintech alternatives. But the data tells a different story: debit is deeply embedded in how consumers fund everyday life and recurring obligations. In fact, 78% of consumers use debit to pay bills, 88% use it for subscriptions, and 95% of consumers have at least one debit card. Debit is also operating at massive scale, with $4.85T in total US debit card volume in 2023, reinforcing that it’s no longer a secondary option, but a powerful and versatile payments credential.

And for billers, debit represents a massive, and often overlooked, opportunity to improve payment success rates, reduce back-office costs, and elevate customer satisfaction in an increasingly digital, always-on bill-pay environment. When debit is presented as a first-class option across web, mobile, IVR, and agent-assisted channels and increasingly through tokenized mobile wallets, it can help more customers complete payments on the first attempt, with fewer exceptions to research and resolve. The result is a better experience for customers who want speed and control, and better performance for billers seeking more predictable cash flow and lower operational friction.

Why consumers are turning to debit in record numbers

Debit’s resurgence isn’t driven by a single trend; it’s the result of several forces converging at once. It has become a daily habit for everyday spending and recurring payments; it aligns with younger consumers’ desire for financial control, and it increasingly sits behind the mobile-first wallet experiences consumers use everywhere.

For billers, these forces translate into a clear mandate: debit needs to be designed into the experience, not treated as an afterthought. When customers are already using debit for day-to-day spending, looking for control over budgets, and paying through wallet-driven, mobile-first journeys, bill pay must meet them with low-friction, debit-forward options across every channel. Done well, that can mean fewer failed attempts, fewer exceptions to resolve, and a more consistent experience that keeps customers coming back.

You can see these shifts in the way people actually pay. Debit is often the “default card” consumers keep on file for essentials like utilities, telecom, insurance premiums, and streaming services. It’s also the card many people choose for everyday spending categories where budgets are top of mind , like groceries, fuel, and quick-service dining, because the money comes out immediately and feels easier to track. And as wallets become the front door for payments, debit frequently sits behind tap-to-pay at retail and in-app checkout, as well as peer-to-peer transfers and cash-management apps that emphasize real-time balance awareness.

Debit aligns with real-life spending behavior

According to internal ACI data, debit isn’t something consumers use occasionally; it’s how many people manage everyday spending. Active debit cardholders complete about 35 transactions per month, reinforcing debit’s role as a true day-to-day habit. For households navigating tight budgets, debit is even more essential: lower-income consumers rely on it nearly twice as often as higher-income households. That real-time visibility helps people manage cash flow and avoid surprises.

That every day, habit-driven usage shows up in independent research as well. The Federal Reserve’s Survey and Diary of Consumer Payment Choice (SCPC/DCPC) ,based on October 2024 data and published in May 2025, indicates debit cards accounted for about 30% of consumers’ payments in 2024, nearly matching credit cards (35%) and far outpacing paper-based methods, underscoring how routinely consumers reach for debit across everyday purchase types.

A generational shift toward financial control

According to internal ACI data, younger consumers, especially Gen Z and Millennials, consistently prefer debit because it helps them stay out of debt. Shaped by economic uncertainty, student loan burdens, and high interest rates, many view debit as the more “responsible” way to pay. It’s familiar, predictable, and transparent, offering spending power without the risk of revolving balances.

That preference shows up in broader consumer research, too. PYMNTS.com found that debit is the preferred online payments option for nearly six in 10 Gen Z consumers and noted this may reflect younger shoppers’ desire to avoid debt. For billers, this matters: offering debit prominently meets younger customers where they already are and reinforces the sense of control they’re looking for when paying essential, recurring expenses.

Sources: Federal Reserve DCPC: https://www.federalreserve.gov/consumerscommunities/diary-consumer-payment-choice.htm; Federal Reserve SCPC: https://www.federalreserve.gov/consumerscommunities/survey-consumer-payment-choice.htm; Mastercard Global Cards and Payments 2024 Market Report (Americas) (subscription); Javelin North American Payments Insights (Dec 2023) (subscription).

Those numbers help explain why debit is also the credential powering many mobile-first experiences.

Debit quietly powers the mobile-first era

These same “control and convenience” preferences are being amplified by the way consumers now pay: through mobile wallets and in-app experiences that make debit fast to select and easy to authenticate. Most shoppers now fund their favorite mobile wallets: Apple Pay, Google Wallet, PayPal, Venmo, and Cash App using debit as their default payment method. Debit’s ubiquity, immediate funds availability, and compatibility with mobile authentication make it the engine behind today’s tap-and-go, tokenized, mobile-first payment experiences.

In a recent ACI blog post, The modern debit card: the engine behind seamless payments, Pierce English noted that debit is now “the silent engine behind mobile wallets, network tokenization, biometric checkout, and the next generation of always-on, API-driven payment experiences.” In other words, the wallet may be the interface, but debit is often the credential underneath, supporting device-based authentication, tokenized credentials that reduce exposure of card details, and the continuity consumers expect when they tap to pay or store a card on file.

Security and trust matter more than ever

With PIN protection, EMV chips, tokenization, biometric wallet authentication, and real-time alerts, debit offers powerful built-in security. Consumers trust debit because it’s straightforward: they know where the money is coming from, and they see it reflected instantly in their account. That transparency builds confidence and confidence drives usage.

Why debit benefits billers as much as consumers

Debit is a win for customers and a practical lever for billers to improve cash flow, reduce exceptions, and manage acceptance costs.

- Higher payment success rates (especially for urgent payments)

Debit reduces failures tied to invalid account details and helps confirm available funds at the time of authorization, resulting in fewer returns and fewer disruptions to cash flow. The urgency behind getting payments through successfully is rising: the ACI Speedpay 2026 Biller Impact Study found that only 42% of billers currently offer an urgent or immediate pay option, and among those who don’t, 82% plan to add it soon. - Faster settlement and better liquidity

Card-based debit supports quicker confirmation and predictable settlement compared to paper checks and many bank-transfer workflows, helping accelerate cash application and reduce days sales outstanding (DSO). - Less back-office work and fewer exceptions

ACH returns and exception handling can create manual follow-up across billing ops and support teams; debit can reduce exception volume and provide structured chargeback processes when disputes occur. According to a 2024 Nacha report, ACH return-rate and exception tracking is a core operational consideration for ACH originators and receivers. - Lower and more predictable acceptance costs than credit

For many US billers, regulated debit interchange is capped for covered issuers (e.g., 21¢ + 0.05% + up to 1¢ fraud-prevention adjustment under current Regulation II), often making debit more economical than credit before factoring in operational savings, according to the Federal Register.

The bigger picture: debit as a strategic asset in modern bill pay

Debit is no longer just a payment method, it’s an indispensable component of a well-designed bill payments ecosystem, sitting at the intersection of customer experience, financial control, and operational efficiency.

For billers, leaning into debit helps you:

- Meet customers where they already are

- Reduce friction and exceptions that drive avoidable costs

- Boost satisfaction and retention with a more predictable payments experience

- Improve cash-flow performance with more successful payments

- Strengthen digital adoption across web, mobile, and agent-assisted channels

- Enable wallet-ready debit experiences (tokenization and modern authentication) that make paying feel effortless

Combined with mobile wallets, real-time payments, digital reminders, automated billing options, and flexible digital channels, debit becomes a foundational pillar of a modern, resilient bill pay strategy, especially when it’s orchestrated end-to-end through platforms like ACI Speedpay to reduce friction, support tokenized credentials, and help customers complete payments quickly and confidently.

Conclusion: The time to prioritize debit is now

As consumer expectations rise and the cost to serve comes under greater scrutiny, debit offers a rare win-win: better outcomes for customers and better economics for billers. The bill-pay leaders won’t treat debit as a fallback option; they’ll design it, using debit-first and wallet-ready experiences to drive higher payment completions, fewer exceptions, and stronger cash-flow performance. ACI Speedpay helps billers operationalize that strategy across channels by orchestrating secure, tokenized debit payments and modern authentication to make paying fast, simple, and dependable.

With ACI Speedpay, billers can operationalize that strategy across channels—web, mobile, IVR, and agent-assisted. ACI Speedpay helps you make debit and wallet-based payments easy to choose, easy to authenticate, and easy to complete. With tokenization support, secure credential storage, and orchestration designed to reduce friction at checkout, billers can increase successful payments, improve on-time behavior, and deliver the fast, modern experience customers expect when every payment feels like tap-and-go and the consumer will never miss a payment.

Want to explore how debit can improve your payments experience, lower operational costs, or increase on-time payments? ACI can help you design a debit-forward strategy powered by ACI Speedpay, that meets your customers’ needs and supports your growth goals.

Debit is already how customers want to pay—are you making it easy?

When debit isn’t easy to find or use, payments fail, customers abandon, and costs rise. Discover how lenders can improve payment success rates, reduce friction, and capture more everyday payment volume by treating debit as a first‑class option.

Amy Kelly is Director of Processing Services at ACI Speedpay, where she leads card processing services and partners with card brands and merchant processors to help billers increase adoption and optimize performance. With 20+ years in the bill payments industry, she brings deep expertise in card processing rules and programs and is known for helping stakeholders navigate complex payment requirements.