As cryptocurrency payments in the merchant sector become more established, and merchants consider offering crypto as a way to pay, they will also be asking themselves if transactions are secure enough for everyday payments. In this blog post, we look at the safety nets that stop crypto becoming kryptonite for those eager to attract the blockchain generation.

The growth in popularity of crypto suggests it is here to stay. Despite initial skepticism, many major players are aligning their commerce strategies accordingly.

Visa, Mastercard, Square and Paypal now offer cryptocurrency integrations so merchants can accept crypto payments from shoppers (e.g., Nexo card). Meanwhile, financial institutions are diversifying and entering the Web 3.0 domain (55 of the top 100 banks have invested in crypto or blockchain companies), and globally, governments are looking at central bank digital currencies (CBDC), with 10 countries already having launched their own CBDCs.

Giving consumers preferred checkout options

As their use of and exposure to cryptocurrency increases, more consumers will want the option to pay for everyday items with crypto.

Already, consumers are making payments with digital currencies like bitcoin at POS and online checkout. In the U.S., more than 46 million users stated they would use crypto to make a purchase in 2021. In addition, in a global survey conducted in 2021, almost 50 percent of Gen Z respondents said they would prefer half of their salary to be paid via crypto.

Why are consumers open to changing the way they pay? Reasons range from “it’s where they’re investing,” and fear of missing out, through to purchase anonymity and obtaining tokens for digital assets.

Security is also a key driver for crypto commerce

Cryptocurrency was built with security and data protection in mind – the word “crypto” literally means concealed or secret. But how does it work in practice?

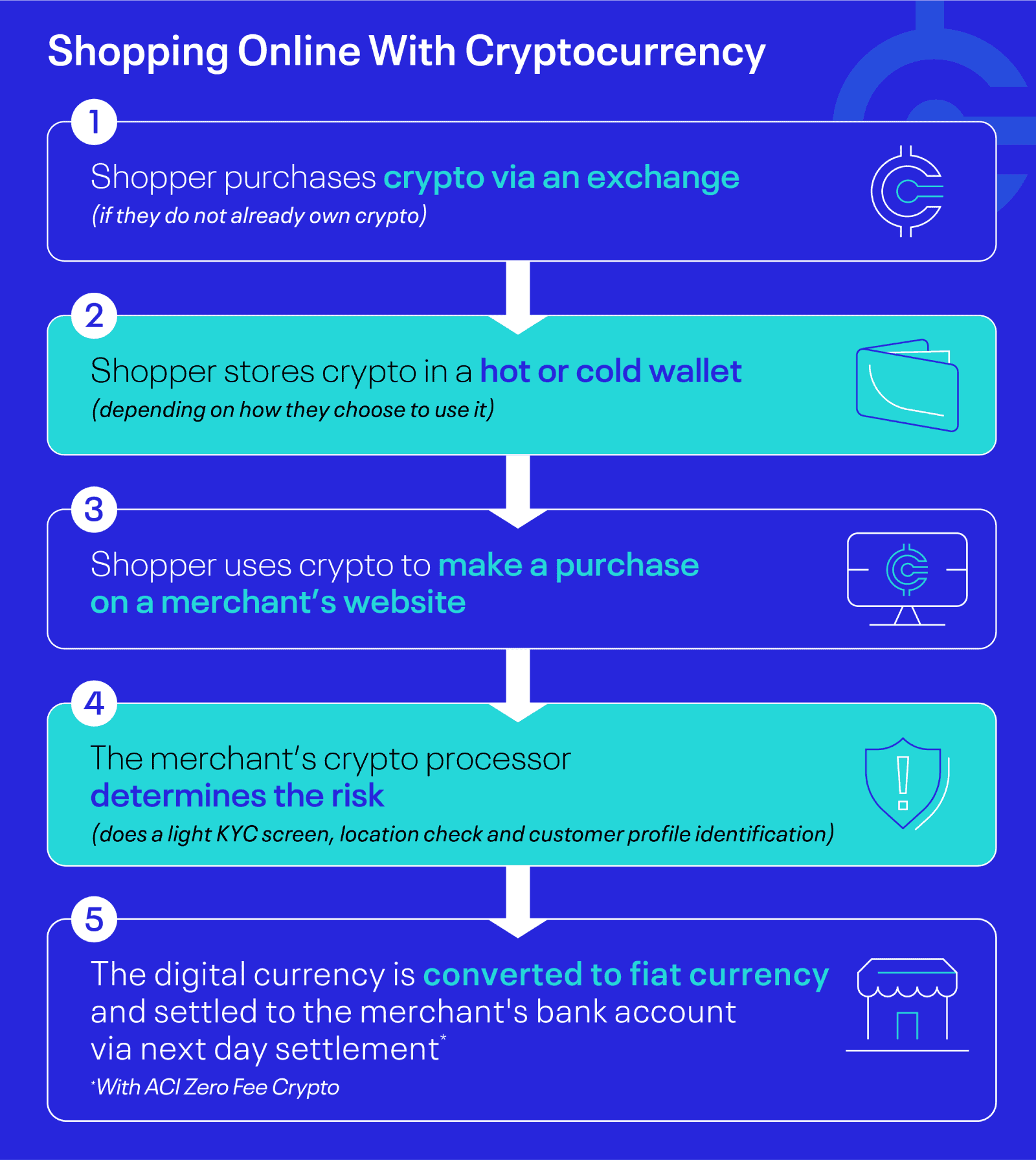

Consumers can buy cryptocurrency with fiat currency on cryptocurrency exchanges. But to store, send and receive digital currency, users need a digital wallet. Merchants also need a digital wallet to accept payments. There are two main types:

- Hot wallets – Also known as software wallets, these are always connected to the internet and are fast and convenient to use

- Cold wallets – Also known as hardware wallets, these are stored offline, making them less convenient, but more secure

These wallets contain the cryptocurrency keys that allow the user to access their coins. This includes a public key (the wallet address which is used to receive funds) and a private key, which is used to “sign” transactions and prove the user owns the related public key.

The use of keys means that when making an online transaction, the shopper does not have to provide any personal or sensitive data, such as name, email and address. This increases privacy and reduces the chances of identity theft. At the same time, the blockchain concept that underpins many major cryptocurrencies ensures a tamper-proof record of all transactions because there is no single point of failure.

How merchants can stay safe when accepting cryptocurrency

The nature of crypto security means that transactions are irreversible. For merchants, this effectively reduces the possibility of fraudulent chargebacks, especially for those operating in high-risk retail sectors.

But how can merchants assess risk? Every crypto transaction is accompanied by metadata (the public key), which remains on the public ledger. This enables transactions to be tracked without revealing a shopper’s sensitive data and makes it much easier to identify a risk transaction versus a genuine transaction for cryptocurrency payments.

In addition, crypto payment processors also carry out multiple credibility checks to help spot suspicious transactions, including:

- KYC (know your customer) – enables cross-validation checks, including running shopper credentials against an anti-terror and money laundering lists

- KYB (know your business) – cross checks the merchant before sending payments to a merchant

- KYT (know your transaction) – running the wallet credentials against sanction lists

What happens if a fraudster targets a crypto transaction?

With crypto, each reputable wallet login is accompanied with two-factor authentication (2FA); for instance, a one-time passcode (OTP) or biometric authentication. If fraudsters get hold of a user’s personal device that contains their wallet, as long as consumer’s phone is protected, the wallet should be too.

Some additional upcoming technologies within the blockchain environment include “sharding”, or sharing just shards of the private key across nodes, which together forms the private keys. MPC, or multi-party computing, is another upcoming technology, which divides the shopper’s key into multiple parts (based on stakeholder), making the key completely invisible to fraudsters.

With these technologies falling into place, merchants will now have the ability to either convert the currency into fiat, or leave digital currencies in their wallets, without having to worry about a compromise.

It’s time to change security perceptions

Despite the higher level of security, more than half of business owners (59%) are still wary of cryptocurrency payments and feel that they are not as safe as credit cards. However, merchants that are already offering crypto transactions generally feel it is a much safer option than other payment methods.

There appears to be a disconnect between actual risk and perceived risk, which means merchants may be holding themselves back unnecessarily. They are they missing out on lower chargebacks and less fraud, but also may not take advantage of benefits offered by some providers, such as “zero-fee” transactions.

Accepting crypto could help them lower transaction costs and open the door to a growing number of consumers that want to transact digitally.

Ready to take the plunge?

If you’re a merchant considering adding crypto payments to your checkout options, here are three ways to minimize risk and keep crypto commerce safe:

- Ensure the payments department is educated about receiving payments with crypto – how it works, what to watch out for and the checks that need to be carried out

- In certain cases, avoid refunds on different wallets; if you receive a request, touch base with your payments processor or verify the genuine-ness of that request

- Chose a payments gateway and partner that can smooth the way to crypto; at ACI, we offer cross-border, cross-channel or cross-platform payments, which includes accepting 120+ crypto coin options globally. Hassle-free, with one click, to ensure optimum conversion

Discover how easy it is to accept crypto safely with ACI