On this page

For fuel and convenience retailers, the customer journey has expanded far beyond the physical pump.

What used to be a simple transaction is now a web of interactions across forecourt terminals, in‑store POS systems, restaurant counters, loyalty engines, mobile apps, EV chargers, and eCommerce sites.

Each one of these touchpoints carries its own payment flows, security requirements, customer data, and loyalty logic. When they operate in isolation, retailers feel the impact immediately—through higher costs, operational complexity, compliance exposure, and inconsistent customer experience.

Where’s the big issue? In recent years, retailers have been pushed to modernize rapidly. Customer expectations are shifting toward speed, digital engagement, seamless transactions, and channel flexibility. All this, while retailers face tight margins, legacy payments infrastructure, and growing regulatory demands. Add in the rising threat of fraud across channels, and the payments landscape becomes even more complicated.

This complexity isn’t just operational; it’s deeply connected to revenue and loyalty. Payments form the underlying fabric of the customer journey, and when those payment touchpoints don’t align, the experience fractures. Customers notice when loyalty doesn’t apply everywhere, or when checkout processes vary by location. Retailers notice, too, through the cost of reconciling multiple systems, inconsistent reporting, and the difficulty of deploying new offers or making changes across the payments stack.

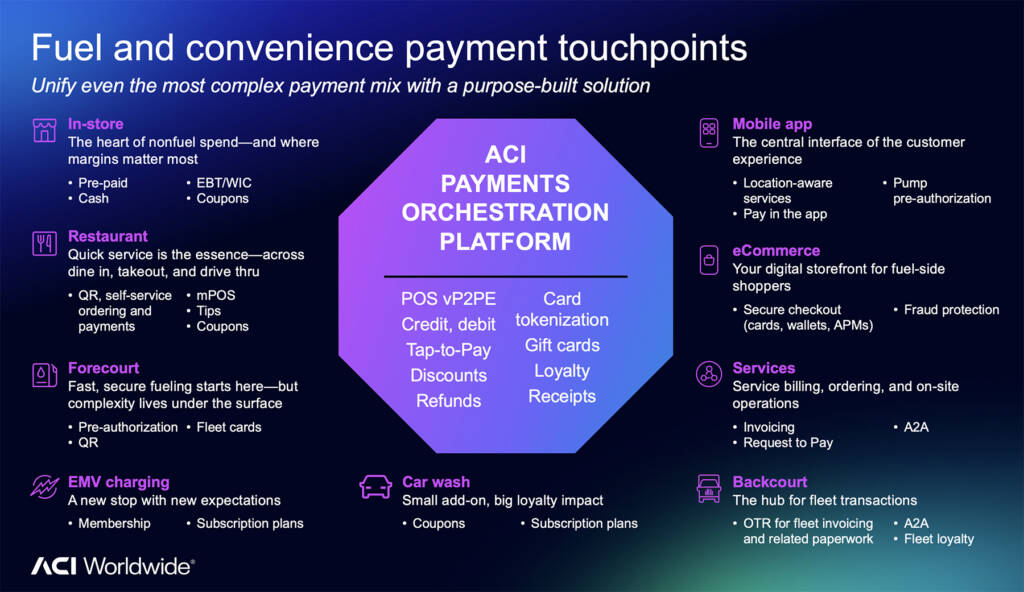

Where payments show up across the modern fuel site

Across any given site, payments appear in more places than most operators realize. First, let’s review what’s considered table stakes across touchpoints: POS vP2PE, card tokenization, credit, debit, gift cards, tap-to-pay, loyalty, discounts, receipts, and refunds.

Think of it as a digital proxy:

At the forecourt—the core of the site—fueling relies on fast pre‑authorization, fleet card acceptance, loyalty recognition, and reliable device‑level security, like validated point‑to‑point encryption (vP2PE). Small delays here ripple across throughput and customer satisfaction.

Inside the store—the heart of nonfuel spend—is where the highest-margin transactions occur. Here, payment options expand even further: debit and credit, tap-to-pay, electronic benefits transfer (EBT)/women, infants, and children (WIC), gift cards, loyalty, discounts, and physical receipts. In‑store POS is often modern, but not always integrated with forecourt, EV, or mobile app data.

The restaurant or QSR adds its own ecosystem: QR ordering, mPOS terminals, tipping workflows, coupons, and loyalty activation. Without integration, this becomes yet another island of data and payments.

Then there are backcourt and services—areas that manage B2B billing, fleet documentation, service shop orders, invoicing, and increasingly digital flows such as Request‑to‑Pay. These processes touch payments just as much as consumer interactions, but often remain manual or disconnected.

On the digital front, eCommerce plays a growing role. Online ordering, pay‑online‑pickup‑in‑store models, digital offers, tokenization, 3D Secure, and fraud controls need to share logic with in‑store and forecourt systems. When eCommerce is handled by a separate provider, consistency becomes even harder.

EV charging introduces a new layer of expectations—membership models, loyalty integration, digital receipts, and secure authentication—often supported by vendors operating separately from traditional fuel systems.

Finally, the mobile app has become the connective tissue of the entire customer experience. It enables location‑aware services, pump activation, tokenized payments, loyalty management, discounts, and increasingly IoT‑driven interactions like automatic vehicle recognition. But without a unified backend, the app becomes just another isolated channel.

Why fragmentation holds retailers back

In every one of these touchpoints, fragmentation drains resources and weakens the customer experience. Unifying them isn’t simply a technological improvement; it’s a business necessity.

Across the industry, retailers face a familiar set of challenges: operational complexity, rising fraud, outdated hardware, inconsistent loyalty, multiple acquirers (or acquirer contracts that are difficult to change), compliance burdens, chargebacks, evolving customer preferences, and the constant pressure to innovate faster while keeping costs stable. Vendor lock‑in and uneven experiences between channels deepen these problems.

When payment systems are fragmented, retailers struggle to:

- Maintain consistent security across channels

- Deploy new payment methods or offers quickly

- Reconcile transactions across multiple providers

- Gain a single view of the customer

- Support fleet and B2B billing efficiently

- Deliver a unified loyalty experience

This fragmentation affects everything from NPS to basket size, authorization rates, and ultimately shrinks revenue.

The value of a unified payments orchestration layer

The solution is a central payments orchestration layer—a single backbone connecting all customer touchpoints. Instead of managing separate systems for the pump, EV charger, store, app, restaurant, and eCommerce site, an orchestration layer harmonizes payments, fraud controls, routing, tokenization, loyalty logic, reporting, and settlement.

With orchestration in place, retailers gain:

- Consistent payments acceptance across all locations and channels

- One secure token and customer identity across pump, app, store, and web

- Central fraud defenses and vP2PE protection

- Unified reporting and dispute management

- Flexibility to introduce new payment methods across the entire estate

- Lower operating costs and fewer integration points

- A connected loyalty experience that reinforces repeat visits

This shift isn’t just technical; it directly enables the goals retailers care most about: Improving customer experience, increasing spend, boosting loyalty, reducing costs, and enabling faster innovation.

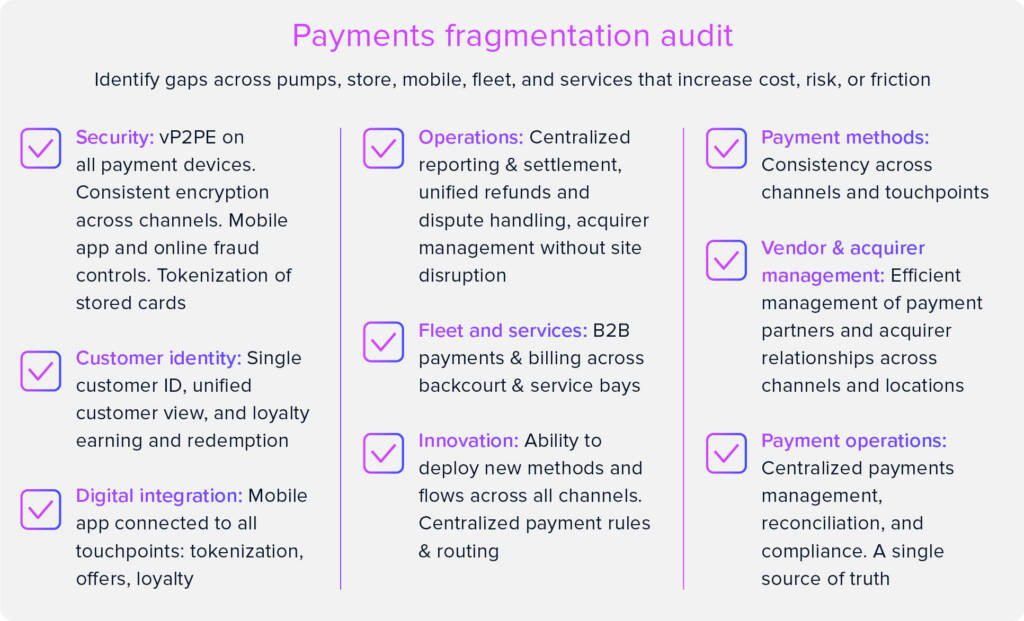

A practical checklist for retailers

To determine whether fragmentation is affecting your operation, ask:

- Security: Is vP2PE deployed uniformly across all payment devices? Are fraud tools and card tokenization deployed?

- Customer identity: Is loyalty recognized and applied everywhere customers transact?

- Digital integration: Do mobile and eCommerce use the same tokens, offers, and customer profiles as in‑store systems?

- Operations: Are reporting, settlements, refunds, and disputes centralized?

- Fleet and services: Are fleet and service operations connected to the broader payments environment?

- Innovation: Can new payment methods, flows, or rules be rolled out across all channels at once?

- Payment methods: Are payment methods consistent across all touchpoints?

- Vendor & acquirer management: Are payment partners and acquirer relationships efficiently managed across channels and locations?

- Payment operations: Is payments management, reconciliation, and compliance centralized with a single source of truth?

If the answer to several of these questions is “no,” fragmentation is likely costing both revenue and efficiency.

Where fuel & convenience retailers go from here

Payments are woven into every corner of the fuel and convenience environment. When those touchpoints operate independently, the experience becomes fragmented, innovation slows, and operational costs rise. But with a unified payments orchestration layer, retailers can connect the entire customer journey—from forecourt to mobile to backcourt—into a seamless, secure, loyalty‑driven ecosystem.

FAQs

Why do payments matter so much in fuel & convenience retail?

Because payments appear across nearly every interaction—fueling, EV charging, in store shopping, food service, mobile, fleet, and online. When those systems aren’t connected, the experience becomes inconsistent, loyalty breaks, and operations get more expensive.

What does “fragmentation” mean in this context?

Fragmentation occurs when different touchpoints rely on separate payment systems, vendors, security tools, and loyalty logic. This leads to mismatched capabilities, separate data sets, manual work, and gaps in reporting and customer identity.

How does a payments orchestration layer help?

It centralizes payments routing, tokenization, security, fraud controls, settlement, reporting, and loyalty logic across all channels. This creates consistency, reduces complexity, and makes it possible to roll out new payment methods or offers everywhere at once.

What are the biggest risks of staying fragmented?

Retailers risk higher fraud and compliance exposure, inconsistent loyalty experiences, slower innovation, complex settlement and reconciliation, multiple vendor dependencies, and lost revenue opportunities—especially as EV charging and digital channels grow.

How does unification improve loyalty?

When all payment channels share the same customer identity and token, loyalty can be earned and redeemed across forecourt, in‑store, app, restaurant, EV charging, and eCommerce. Customers experience one brand, not disconnected systems.

Do we need to replace all existing hardware to unify payments?

Not necessarily. Many retailers modernize gradually by introducing orchestration behind the scenes, while upgrading POS, pump, EV, and service systems over time. A modern orchestration layer supports mixed environments and phased rollouts.

What role does security (like vP2PE and tokenization) play?

Security must be consistent across all touchpoints. vP2PE protects card data in physical environments, while tokenization protects stored credentials across mobile, web, and loyalty systems. Unification ensures no channel becomes the weakest link.

How can we tell if fragmentation is costing us?

Common warning signs include different payment methods accepted in different places, loyalty not working everywhere, multiple settlement files, inconsistent reporting, slow rollouts, and manual workarounds between systems.

What does modernization look like in practice?

In most cases, retailers start by centralizing payments and loyalty, enabling tokenization, connecting mobile and eCommerce channels, and unifying reporting. From there, they streamline fleet billing, upgrade security, and phase in EV and service integrations.

Dan Coates is the director of merchant product management for ACI Omni-Commerce with over 25 years of payments experience. He focuses on solution use-cases, insight and thought leadership for merchant retail in the card present, eCommerce and mCommerce space. Dan has led payments implementations for major retailers, developed payments software for ACI’s Omni-Commerce platform, and implemented large scale projects for many top global brands. His earlier roles at ACI include senior lead positions in engineering, architecture, consulting, and solution evangelist.