On this page

Alternative payment methods (APMs) are no longer a “nice to have.” In many markets, especially across LATAM and APAC, they’re a baseline expectation. When implemented well, they can significantly boost conversion, authorization rates, and customer satisfaction.

But adding APMs comes with risk. Too many merchants roll out new payment methods simply because competitors do, only to introduce checkout friction, operational complexity, or hidden costs that undermine performance.

The key is to treat APMs as performance levers, not feature additions. Below are five practical principles to help you implement APMs in a way that drives real business impact.

Start with customer preferences, not assumptions

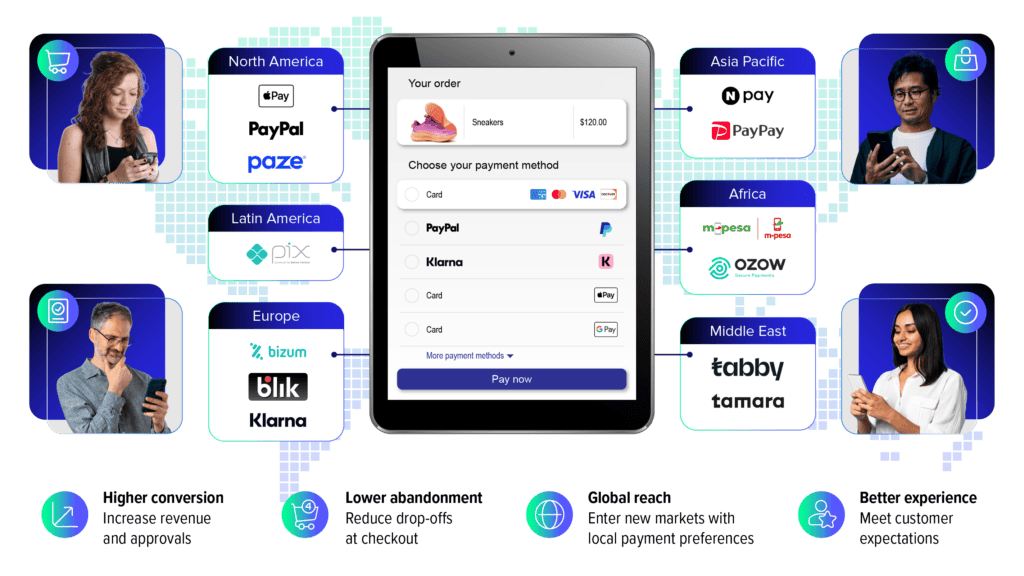

Before adding any alternative payment method, base your decisions on real customer data. Payment preferences vary significantly by geography, device type, and demographic profile.

For example:

- Customers in Europe often expect SEPA Direct Debit and PayPal

- Shoppers across APAC commonly adopt regional wallets such as Alipay or GrabPay

- Mobile-first audiences tend to favor wallets and tokenized methods over manual card entry

Analyzing where your customers are and how they prefer to pay helps you prioritize the APMs most likely to drive adoption and conversion. Assumptions create clutter. Data creates impact.

Choose APMs that reduce friction and boost conversion

Not all APMs improve conversion. Some simply add noise. Prioritize payment methods that:

- Speed up checkout

- Require minimal input

- Deliver higher authorization rates

Wallet-based and tokenized APMs consistently outperform manual-entry methods. If an APM doesn’t measurably reduce friction, it doesn’t belong in your checkout.

Ensure strong fraud and risk controls

Alternative payment methods vary widely in how they handle fraud, disputes, and liability. Some include strong built-in protections, while others shift risk back to the merchant. Before launch, confirm:

- That your existing fraud tools support the APM

- How refunds, chargebacks, and disputes are managed

- If liability shift applies and under what conditions

Strong risk controls protect revenue while preserving approval rates. Understanding these details upfront prevents costly surprises as transaction volumes grow.

Give customers the payment options they want

ACI helps merchants simplify and optimize alternative payment strategies by offering payments orchestration, global APM coverage, and integrated fraud management. This allows merchants to activate the right payment methods by market, monitor performance in real time, and adapt quickly as customer preferences evolve without adding unnecessary operational complexity.

Test and optimize end-to-end checkout experiences

Successful APM implementation goes beyond technical integration. The real measure of success is how the payment method performs within the full checkout experience. Be sure to:

- Validate flows across devices and browsers

- Monitor load times and error handling

- Ensure compatibility with existing UX, analytics, and reporting

Whenever possible, use A/B testing to confirm that an APM improves conversion rather than introducing noise. A well-integrated alternative payment method should feel natural to the shopper.

Monitor performance and improve continuously

Once live, track APM performance like any mission-critical checkout capability. Track performance using key metrics such as:

- Adoption rate

- Checkout abandonment

- Authorization and settlement rates

- Cost per transaction

- Refund and dispute patterns

Regular optimization ensures each APM continues delivering value and aligns with evolving customer expectations.

Turning alternative payment methods into a competitive advantage

Adding more payment methods does not automatically improve checkout performance. The merchants that succeed with APMs focus on relevance, execution quality, and continuous optimization.

When implemented with intent, APMs do not complicate checkout. They make it faster, safer, and more aligned with how customers want to pay.

Used strategically, APMs become a true competitive advantage, not just another line item in the checkout.

FAQs

Do alternative payment methods apply only to online payments or also to in-store?

APMs apply to both online and in-store environments, although adoption differs by channel.

- In eCommerce, APMs such as wallets (e.g., PayPal, Apple Pay), bank transfers (e.g., iDEAL in the Netherlands, now Wero as an emerging pan-European alternative), and BNPL options (e.g., Klarna) often reduce friction and improve conversion.

- In physical retail, mobile wallets (e.g., AliPay) and QR-based payments (e.g., WeChat Pay QR codes) are increasingly common, particularly in APAC and parts of Europe.

A unified payments strategy helps ensure consistency across online and in-store experiences, especially for omnichannel merchants.

How many alternative payment methods should a merchant offer?

There is no universal number. More payment methods do not automatically lead to higher conversion. Most merchants perform best when they:

- Offer a curated set of highly relevant APMs

- Focus on methods with proven adoption and performance

- Regularly review usage data and remove underperforming options

Clarity at checkout is often more effective than excessive choice.

How long does it take to implement a new alternative payment method?

Implementation timelines vary by payment method, region, and internal stack complexity. Factors that influence rollout speed include:

- Integration approach and orchestration capabilities

- Fraud and compliance requirements

- Checkout and UX adjustments

- Testing and certification processes

Using a modern payments platform can significantly reduce time to market by standardizing integrations and workflows and decreasing compliance burden.

How can merchants measure the success of an alternative payment method?

Merchants should evaluate APM performance using the same rigor as card payments. Key success metrics include:

- Adoption and usage rates

- Checkout abandonment and conversion impact

- Authorization and settlement success

- Cost per transaction

- Refunds, chargeback, disputes, and fraud rates

An APM should demonstrate clear value within a defined timeframe or be reoptimized or retired.

Transform your customers’ retail payments experience

ACI offers merchants a unified payments platform that simplifies APM implementation across markets.

With payments orchestration, global APM support, embedded risk controls, and real‑time performance monitoring, merchants can launch new payment methods faster, reduce checkout friction, and continuously optimize payments performance without increasing operational complexity.

Corina Filipas is an ACI Worldwide payments expert focused on helping merchants scale and optimize their eCommerce businesses. She specializes in global expansion and strategic eCommerce initiatives, enabling the right mix of payment methods and improving authorization performance across diverse markets. With deep expertise in digital commerce and merchant ecosystems, she is known for turning complex payment challenges into clear, practical strategies that accelerate growth, enhance customer experience, and unlock new market opportunities.