On this page

Tuition payments used to be treated like pure back-office plumbing: necessary, routine, and largely invisible unless something broke. In 2026, that mindset no longer fits reality. Paying for college is one of the highest-stakes transactions most families make, often repeated several times per term, sometimes by more than one payer, and frequently alongside financial aid, installment plans, and refunds. That combination turns “how we pay” into part of the student experience, not just an administrative step.

In my view, the shift is straightforward: digital is now the default, but families haven’t stopped caring about control, trust, and flexibility. Those needs shape which payment options they use and whether they feel confident that a payment “worked” after they click Submit. Underneath all of it is a quieter requirement that doesn’t show up in feature checklists: resiliency. In a high-stakes moment like tuition, the best outcome is boring—payments that go through, post predictably, and help families never miss a payment, even when something changes or goes wrong.

Five patterns I’m seeing in tuition payments

- Digital is the baseline, but it’s not universal. Digital preference is strongest among younger payers and lower among older ones. My takeaway for campuses: design digital-first, not digital-only.

- Tuition is a commonly shared responsibility. Payments are often split across students, parents, and sometimes third parties. That makes authorized payer workflows and role-based notifications essential, not “nice to have.”

- Bank rails still anchor tuition. Checking/ACH remains the workhorse method, while cards and wallets play supporting roles. Convenience may drive adoption, but trust and cost shape which rails people pick.

- Convenience matters, but trust and fees are close behind. Ease leads to the initial choice, but people quickly evaluate whether the option feels safe and whether the fees are worth it. Younger payers, for example, are more likely to balk at added costs.

- Autopay is popular, but people still want control. Many families like automation, but they also want visibility into what will draft, when it will draft, and simple ways to pause or stop it. In other words, autopay doesn’t mean “hands-off”; it means “don’t make me start over every month.”

Below, I’ll unpack a few of these patterns with supporting data and practical implications for bursar, student accounts, and finance teams.

Digital-first is now table stakes, but “digital-only” is a mistake

It’s tempting to read “digital is the default” and conclude that the work is simply to add Apple Pay, enable eBilling, and move on. But in my experience, the generational split in payment preferences, higher digital comfort among Gen Z and lower among older payers, doesn’t just track age. In tuition payments, it often tracks roles. Students tend to optimize speed and mobile convenience; parents tend to optimize reassurance, error recovery, and auditability.

That dual-audience reality is consistent with broader higher education research on student-facing digital services. For example, the 2025 EDUCAUSE Students and Technology Report shows that students increasingly expect convenient, technology-enabled self-service in their campus experience. In the billing and payments context, that translates into a portal that is easy to find, easy to use on mobile, and clear about what happens next, because the expectation for modern digital workflows doesn’t disappear just because the transaction is “tuition” instead of “retail.”

Here’s the practical takeaway I keep coming back to: modernizing tuition payments isn’t about nudging every family into the newest payment method. It’s about getting the first digital experience right and making sure there are reliable, low-friction fallback options when real life shows up. In a great setup, the portal and mobile flow feel fast and obvious, and the “I need another way to pay” paths (ACH, checks where required, and assisted support) are easy to find without having to search extensively. That’s not just about preference; it’s about resiliency. The whole point is to help families finish the transaction on time and with confidence, so they don’t miss a payment because one option failed, a balance changed, or they couldn’t figure out what to do next.

And when that resiliency isn’t there, when the system is vague about what happens next, people do what they always do with high-stakes bills: they call. They’re trying to confirm the payment went through, understand why the balance hasn’t updated, avoid late fees, or prevent a duplicate payment from a well-meaning second payer. That single call carries real cost: Gartner’s 2024 customer service benchmarks identify the median cost of an assisted support contact (phone, chat, or email) at $13.50. On campus, it also pulls staff into manual research, creates back-and-forth follow-ups, stretches hold times during peak periods, and increases the odds of rework (voids, reversals, refunds, and account adjustments). In other words, a “small” UX gap quickly becomes a real operational cost.

Design for multi-payer tuition

One of the most actionable insights in ACI’s 2026 Higher Education Payment Trends Report is how often tuition is paid collaboratively. If nearly eight in 10 Gen Z respondents share responsibility, identifying the payer is no longer straightforward. It might be a student paying from a checking account, a parent covering a remaining balance by ACH, and a third party contributing through a payment plan, sometimes all in the same billing cycle.

That’s why multi-payer support must be engineered as a first-class workflow: simple authorized payer invitations, clear role-based permissions, shared visibility into balances and due dates, and notifications that go to the right person at the right time (statement ready, upcoming due date, autopay draft scheduled, payment receipt). The goal isn’t just a nicer UX, it’s fewer “Did you pay?” text messages, fewer duplicate payments, and fewer calls that begin with “I’m looking at the portal, and it doesn’t match what my daughter told me.”

More importantly, better multi-payer design doesn’t have to trade off with compliance or controls. In fact, it can strengthen them: audit trails for those who initiated a payment, confirmation that an authorized payer saw fee disclosures, and a clean history of notifications and receipts can reduce disputes and streamline exception handling. Done well, “front-door” convenience becomes a back-office efficiency lever.

Trust is visibility: posting, receipts, status

When families tell me they care about “trust,” they’re almost never asking about encryption standards or payment network architecture. They’re asking the very human questions: Did it go through? Did the balance change? If something looks off tomorrow, will I be able to prove what happened?

That’s why one line in the 2026 Higher Education Payment Trends Report jumped out at me: real-time (or near-real-time) posting is becoming a “trust signal.” You can feel that in the day-to-day experience. When a payment is submitted but the student account doesn’t update, families assume something went wrong, even if everything is technically “processing.” Then the follow-ups start: emails, portal messages, and, eventually, phone calls. Meanwhile staff are pulled into manual transaction research, and peak billing weeks get louder than they need to be. A few simple product choices go a long way here, clear “posted vs. pending” status, instant receipts, and proactive messaging about timing, because they remove ambiguity before it turns into a call queue.

And honestly, this isn’t unique to higher ed. In the broader bill-pay world, the things people associate with a “good” payments experience are consistent: it’s reliable, it’s easy, and it tells you what’s happening. Tuition just raises the stakes. The dollar amounts are bigger, the consequences are more stressful, and more than one person may be involved, so the expectation for clear confirmation and predictable status only gets stronger.

Convenience matters but cost and flexibility drive adoption

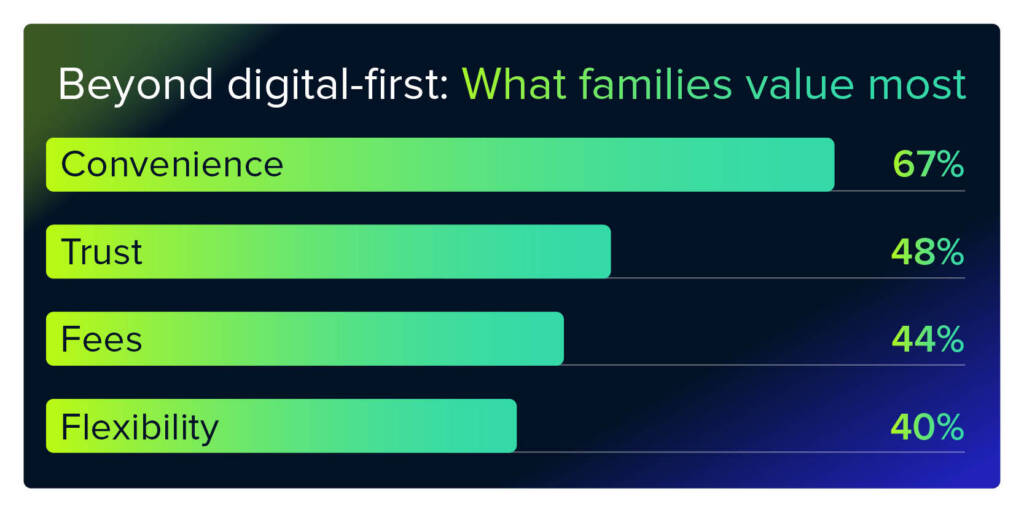

When I watch how families choose a way to pay, I’m reminded that “convenience” is only the first filter. In the survey data1 I’ve been looking at, convenience still comes out on top (67%), but trust (48%) and fees (44%) are right behind it, and flexibility (40%) is far from a rounding error. That tracks with what you see in the real world: people gravitate to the option that feels easiest, least risky, and most sensible for their budget and timing.

Two nuances are easy to miss if you haven’t watched families navigate this in the wild. First, in tuition, balances change, so anything that looks like “set it and forget it” can feel risky unless there’s clear visibility into what will draft, when it will draft, and how to stop it. Second, when people say they want “control,” they don’t all mean the same thing: for some, control is paying in full and being done; for others, it’s having a predictable plan they can budget around.

One pattern I don’t think campuses can afford to gloss over: younger payers (Gen Z and Millennials) are especially fee-sensitive. That makes the presentation of card payments, convenience fees, and installment plan costs especially important. If the goal is to shift volume toward lower-cost rails (often ACH), the best lever usually isn’t hiding card options or burying the “other ways to pay.” It’s being painfully clear up front, ideally with a simple, side-by-side view of what each method costs and how long it typically takes to post, so families can self-select based on the true cost, without feeling like they were surprised at the last click.

And flexibility isn’t just a nice UX add-on; it’s a response to the underlying economics of how families fund college. Published tuition and fees remain high, and most households are stitching together grants, loans, income, and family support to cover the bill. College Board’s Trends in College Pricing and Student Aid reports (2024 and 2025 editions) make that mix hard to ignore: net prices and financing patterns vary widely, which naturally increases demand for installment plans, scheduled payments, and clear, always-updated visibility into what’s still owed.

Checking accounts still anchor tuition, so optimize ACH instead of treating it as “legacy”

Even as digital wallets and new rails grab headlines, tuition payments are still grounded in familiar bank account behavior. Our 2026 Higher Education Payment Trends Report found that personal checking accounts are the most-used method (48%), with credit and debit next (26% each). That mix makes intuitive sense: ACH is widely trusted, avoids revolving interest, and often carries lower (or no) convenience fees compared to cards.

So, the strategic question for institutions isn’t whether to “keep ACH.” It’s whether the ACH experience is as modern as the campus wants the overall payments experience to be. Optimizing ACH can include streamlined bank-account enrollment, clear eligibility and timing disclosures, saved payment methods, right-sized validation and fraud controls, and, crucially, posting transparency that eliminates the anxious gap between “payment submitted” and “balance updated.” And because payments don’t just flow in one direction, the same clarity matters on the way out: refunds that are easy to enroll in, easy to track, and predictable in timing do a lot to preserve trust.

None of that means campuses should ignore wallets, cards, or faster payments. Consumer adoption of digital options and instant payment services continues to grow (as reflected in recent Federal Reserve and industry studies). But in tuition, these methods work best when positioned as intentional choices: cards for short-term liquidity or rewards, wallets for ease on mobile, and faster rails where the institution can support them operationally. The key is orchestration, offering choice without creating reconciliation chaos or inconsistent posting behavior.

What bursar, student accounts, and finance leaders can do now

- Design for shared payments responsibility by default. Make authorized payer setup simple, provide role-based access, and deliver targeted notifications to reduce duplicate payments and status confusion.

- Treat posting visibility as a product requirement. Make “posted vs. pending” obvious, send instant receipts, and explain timing in plain language. Fewer unknowns mean fewer calls.

- Make ACH feel modern. Streamline enrollment, save payment methods safely, and ensure ACH payments and refunds are trackable with predictable timelines.

- Offer autopay with guardrails. Use draft alerts, clear schedules, easy pause/cancel, and a visible payments history, so automation feels controlled rather than risky.

- Lead with transparency. Make the bill easy to understand: itemize charges, surface due dates, and disclose any fees up front. When possible, show a simple side-by-side comparison of payment methods so families can choose confidently, without surprises at checkout.

- Modernize refunds without removing choices. Keep direct deposit as the dependable default, add faster options where feasible, and preserve check workflows with clear expectations.

Conclusion: Digital is expected; confidence is earned

The tuition payments experience in 2026 is less about novelty and more about confidence. What I see repeatedly is that families expect digital options, but they judge the experience (and the institution behind it) on the basics: is it transparent, does it feel controllable, and can it flex to real life? For campuses, the opportunity is to make payments a front-door experience with back-office rigor: orchestrate choice, modernize the bank-rail default, and use visibility (not guesswork) to reduce stress for families and rework for staff. Digital may be the default, but it’s performance that earns trust. Resiliency is what turns that performance into the promise families care about: don’t let me miss a payment.

1 ACI 2026 Higher Education Payment Trends Report, https://www.aciworldwide.com/higher-education-payment-trends-report

Higher education payments in 2026: How students and parents want to pay

Discover how students and parents want to pay in 2026—and what that means for your billing strategy. This ACI/YouGov research reveals how digital preferences, shared payer behavior, and refund expectations are reshaping tuition payments.

Related content

The need for speed is accelerating

Evolving consumer expectations are redefining digital bill payments and what billers must do to keep up

ACI Speedpay Biller Impact Study: A new era in bill pay has arrived

Discover the strategies and innovations shaping the next era of bill payment

The case for lenders to accept debit card payments

There is a strong, growing consumer preference for using debit cards with bill payments, especially among younger generations

Why modern bill pay requires more than the lowest-cost rail

Billers across industries, from mortgage servicing to credit cards, utilities, and insurance, are actively modernizing their bill pay infrastructure.

The modern debit card: The engine behind seamless payments

Cards continue to play a central role in bill pay and recurring payments, giving customers a familiar, trusted way to complete transactions across channels.

James J. Curry, Jr. leverages more than 35 years of leadership experience in higher education as a new business developer at ACI Worldwide. With a focus on project management and IT implementations that enhance student success, his expertise encompasses academic, administrative, and operational functions. His progressive background in leadership and an advanced educational foundation, help him excel in problem-solving campus commerce payment solutions, leveraging technology to drive efficiency and innovation for institutions.