INDUSTRY guide

EMV Technology and Transactions, Explained

EMV technology empowers merchants to create seamless, secure payment flows for card-present transactions

On This Page

What are EMV payments?

In 1993, Europay, Mastercard and Visa came together with the goal of developing a global secure payments technology standard for processing credit and debit card transactions. Known as EMV, this standard was intended to replace traditional card-present payment verification methods, such as magnetic stripes and mechanical imprints, which had proven less-than-effective against increasingly sophisticated forms of fraud.

In the years since the standard’s introduction, American Express, JCB and UnionPay have joined the founding three members of EMV, forming EMVCo. EMVCo continues to manage EMV payments and develop new specifications based on emerging fraud trends and technological developments.

How does EMV technology work?

EMV technology uses integrated circuit chips rather than magnetic stripes or mechanical imprints to secure payments. These chips — which are embedded directly within debit and credit cards — store encrypted data and generate dynamic transaction codes, making it harder for fraudsters to steal and use cardholder data.

EMV technology is a fairly broad category that encompasses a suite of payment technologies, including:

- EMV contact chips

- EMV contactless chips

- EMV mobile payments

- EMV payments tokenization

- EMV QR codes

- EMV secure remote commerce

- EMV 3D Secure

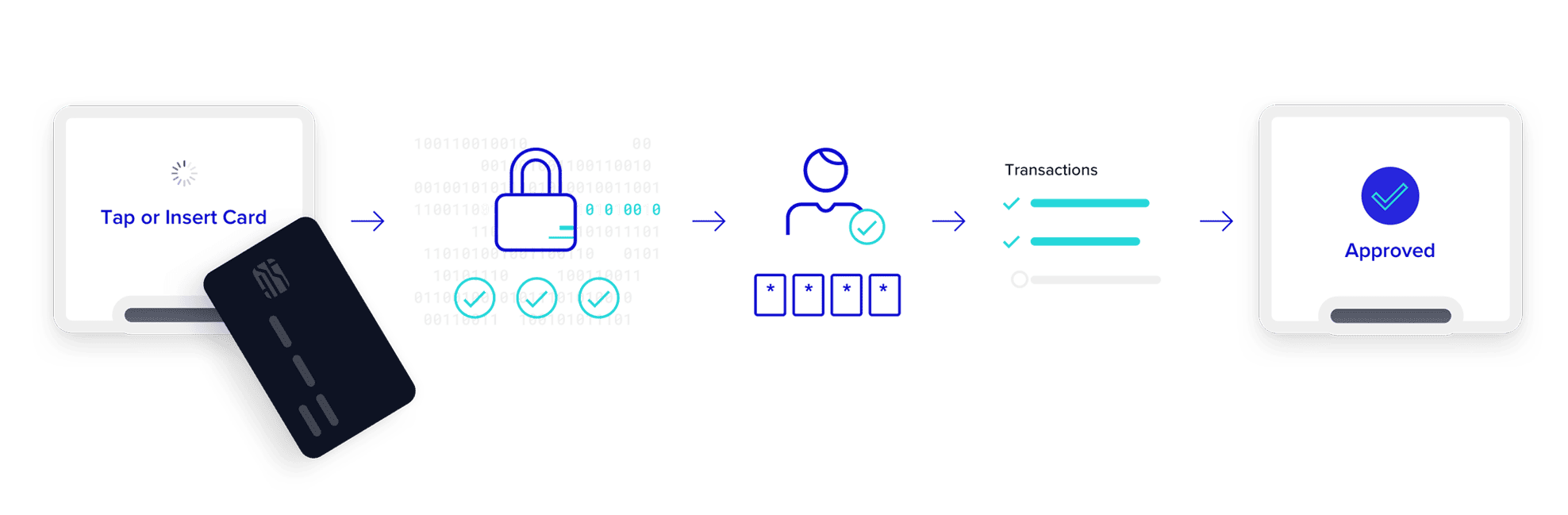

How do EMV transactions work?

- A cardholder inserts their EMV chip card into or taps it against a payments terminal, thereby initiating the transaction.

- The terminal then reads the chip card’s encrypted data and runs a series of cryptographic checks to authenticate that the card hasn’t been tampered with.

- Once the terminal has verified the cardholder’s identity, the EMV chip generates a unique, one-time transaction code and sends that cryptogram, as well as cardholder data and transaction details, to the card issuer.

- The card issuer analyzes the details of the transaction, the cardholder’s risk profile and their available funds to determine whether to approve or reject the transaction.

- If the card issuer approves the transaction, it sends an authorization code to the payments terminal. The payments terminal displays an approval message and prompts the cardholder to remove their card. Funds are transferred from the cardholder’s account to the merchant’s account, thereby completing the EMV transaction.

This entire process takes place in a matter of seconds, creating a fast, frictionless and secure experience for shoppers.

Are all credit or debit cards with chips EMV compliant?

Not all chip cards are EMV cards; some are actually chip and personal identification number (PIN) cards. While both EMV cards and chip and PIN cards use integrated circuit chips for security, the latter also require cardholders to enter a unique PIN to authenticate transactions.

Other key distinctions include that EMV technology is a global standard, whereas chip and PIN technology is primarily used in certain regions, and that chip and PIN cards are more commonly used for debit card transactions, while EMV cards are more commonly used for credit card transactions.

How widespread is EMV technology adoption?

EMV technology has existed since 1993; in the 30 years since its introduction, EMV has seen widespread adoption. According to research from EMVCo, as of Q2 2022:

91.94%

of global card-present transactions used the EMV chip

99.20%

of card-present transactions in Africa and the Middle East used the EMV chip

82.80%

of card-present transactions in Asia used the EMV chip

97.94%

of card-present transactions in Canada, Latin America and the Caribbean used the EMV chip

99.58%

of card-present transactions in Europe Zone 1 used the EMV chip

97.54%

of card-present transactions in Europe Zone 2 used the EMV chip

84.84%

of card-present transactions in the United States used the EMV chip

Are merchants legally required to support EMV payments?

Although merchants are not mandated to support EMV payments, any merchant that does not use the EMV standard could be liable for any fraudulent transactions that take place.

Traditionally, issuing banks were liable for any chargebacks resulting from fraudulent activity due to a lost or stolen card. As fraud evolved, so too did the methods to combat it, including EMV payments. In 2015, major credit card networks introduced a liability shift in an attempt to incentivize merchants to implement EMV technology.

Under this new rule, if a merchant fails to use EMV to authenticate a transaction, and that transaction turns out to be fraudulent, the acquiring bank would be liable. In most cases, the acquirer will pass this cost onto the merchant, essentially making merchants liable for chargebacks. This rule was effective immediately for all merchants, except for fuel merchants, whose EMV implementation deadline was set for 2021.

What are the benefits of accepting EMV payments?

Merchants that implement EMV technology enjoy a long list of benefits, including:

Reduced fraud liability

By supporting EMV payments, merchants substantially reduce their — and cardholders’ — fraud risk exposure. Though merchants are not directly liable for chargebacks resulting from fraudulent, non-EMV transactions, acquirers often pass on the cost of chargebacks to merchants. Therefore, by using EMV technology, merchants can reduce their fraud exposure and mitigate the effects of chargebacks to their bottom lines.

Increased customer confidence

EMV technology builds an additional layer of security into the checkout process, giving cardholders the much-needed peace of mind that their sensitive information is safe when making card-present transactions. By reducing risk to cardholders, merchants can build trust with their customers, which can lead to longer-term loyalty and stronger reputational standing.

Frictionless checkout experience

Although EMV adds a layer of security to transactions, it doesn’t add any complexity to the checkout process. EMV payments are fast and efficient, authenticating cardholders’ identities in a matter of seconds without adding any steps to the checkout process, creating a better overall customer experience.

Access to a global standard

Merchants who adopt EMV can do so with confidence because it is a global standard, meaning it leverages proven and widely adopted technology. Additionally, EMV has been a payments industry standard for nearly three decades and is regularly updated by EMVCo to leverage the latest technological advancements.

Compliance with key regulations

The payments industry as a whole is making a concerted effort to fight fraud, with many regulatory authorities introducing new consumer protection requirements.

For example, the European Commission has introduced the Revised Payment Services Directive (PSD2), which applies to payment services and payment service providers in the European Union and the European Economic Area. PSD2 mandates strong customer authentication (SCA), a form of two-factor authentication, for all merchants. EMV 3D Secure, specifically, meets PSD2’s SCA requirements, making it easier for merchants to stay compliant.

PSD2 and Strong Customer Authentication (SCA): A PSP Guide

Explore the requirements within PSD2 for SCA and why merchants and issuers in the European Economic Area (EEA) are required to validate the consumer for all electronic payments.

How does ACI Worldwide support EMV payments?

Although ACI Worldwide does not explicitly provide EMV technology, our ACI Payments Orchestration Platform and ACI Fraud Management for Merchants solutions deliver enhanced security through smart tokenization, point-to-point encryption and multilayered fraud prevention strategies. When paired with EMV technology, ACI’s solutions can help merchants maintain PSD2 compliance, avoid chargeback liability and create the most seamless and secure shopping experiences for their customers.

To learn more about the ACI Payments Orchestration Platform or our other solutions, contact the ACI team today.