Blog

The women behind Bre-B How collaboration, consensus, and leadership helped transform payments in Colombia

Payments optimization in 2026: 6 stats every retailer should know

Standing still is the real risk in cards. Q&A with cards & payments expert, Dean Wallace

Top five tips for implementing local payment methods

Visa’s service-fee update for utilities: What changes and what doesn’t

Visa added utilities (MCC 4900) to its Service Fee Program. See what changed, how it affects autopay, and how to choose the right fee model.

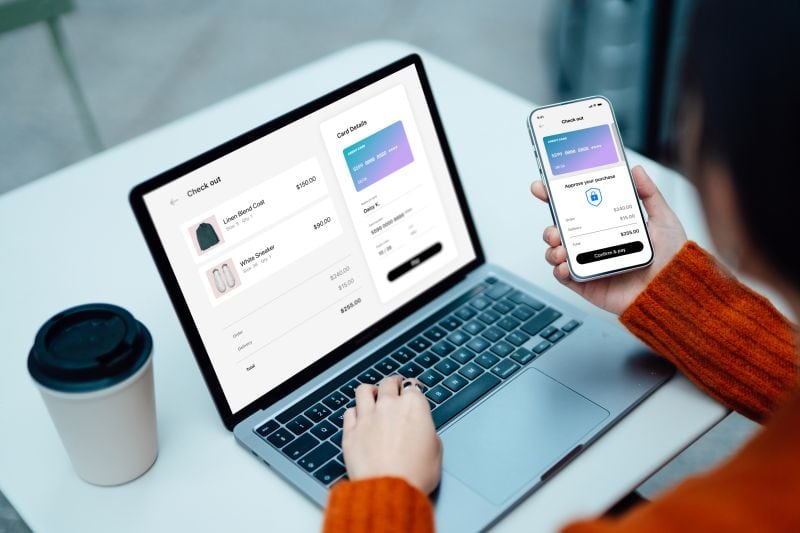

The sales that never post: Christian Schönhuth on recovering margin at checkout

Declines, false positives, and friction erode checkout revenue. Learn how merchants can improve conversion and recover lost value.

Beyond reimbursement: ACI’s Jackie Barwell on stopping APP scams while the money is still in flight

Fraud prevention is shifting. Learn how liability changes and real-time data sharing help banks stop scams before money moves.

Debit is having a moment: Why consumers prefer it and why billers win when they support it

Not offering debit creates friction, failed payments, and higher costs. Learn why debit is essential for improving payment success and cash flow.

The demographic shift powering debit: Why younger, digital‑first customers are choosing it over ACH

Debit is becoming the default for daily spend. See how mobile wallets, habits, and visibility are reshaping payments behavior.

Real-time payments outrun the rules: Craig Ramsey on pay-by-bank and orchestration

Real-time payments are scaling faster than rules. Learn how orchestration, pay-by-bank, and regulation gaps are reshaping bank strategy.

Leadership in an era of transformation

Navigate the future of payments with insights on today’s barriers, leadership strategies, and ecosystem shifts.

Pay-by-bank, tokenization, and the UK national payments vision: Paul Horlock, Santander UK

Santander’s Paul Horlock on UK payments strategy, pay‑by‑bank, and why programmable money—not rails—will define the next phase of growth.

Is your card platform holding back growth? Legacy vs. modern explained

Learn how card platform choices impact cost, speed to market, and revenue, and why modernization is now a critical driver of growth.

When gas prices rise, how can fuel retailers protect traffic and loyalty

Learn how fuel merchants can adapt to rising prices with clearer value, smarter loyalty strategies, and payment experiences that keep customers coming back.

Bet on what’s new or fix what scales? John Dawson on payments innovation, AI, and trust

Payments are moving faster—but trust must keep up. Learn what leaders must solve around AI accountability, fraud, and payments innovation.

Agentic commerce and the trust problem at checkout: ACI’s Adriana Iordan on what breaks when software starts buying

Agentic commerce is reshaping checkout—but trust, fraud, and liability models aren’t ready. Learn what breaks and what merchants must solve next.

Why the health plan payments experience is becoming the new front door for members

Payments shape member trust, retention, and cost. Learn how health plans can reduce friction, improve premium continuity, and modernize member payments.