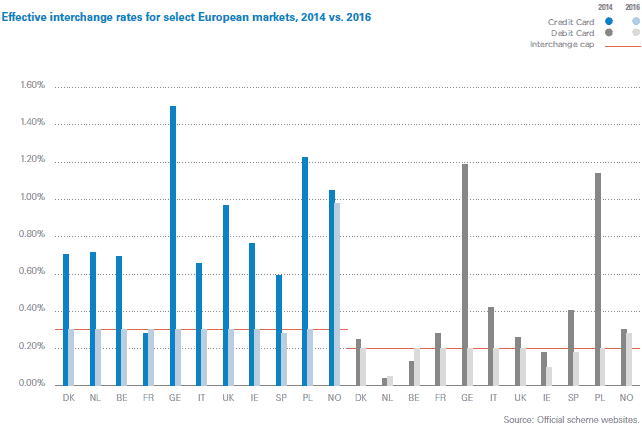

MIF Regulation levels the playing field

As of 9 December 2015, interchange fees in the EU were capped at 0.3% for credit cards and the lesser amount of 0.2% or €0.05 per transaction for debit cards. Individual EU member states are free to mandate even lower caps. However, corporate cards, three-party scheme cards (Amex and Diners are the most prominent examples), and ATM transactions are exempt from the caps. One of the main outcomes from the caps is a level playing field across Europe as fees are aligned. Outliers such as Germany, Poland, and Norway now have rates the same as everyone else.

One likely effect of this cap on interchange rates will be increased card acceptance and usage, particularly in countries that traditionally had higher rates and lower card penetration. The lower rates will encourage more merchants to offer cards and higher acceptance will push more shoppers to use them. However, the caps will affect a number of payment actors in different ways.

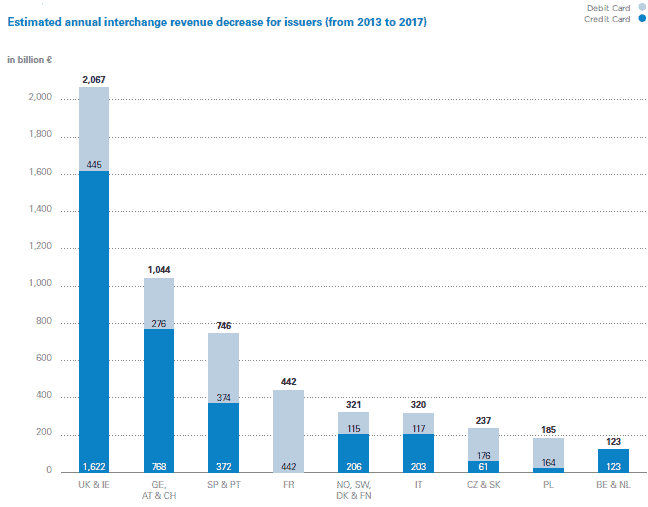

Significant revenue loss for issuers

The 0.3% cap on credit and 0.2% cap (or €0.05 per transaction, whichever is lower) on debit card interchange fees means card issuers face reduced revenues. The markets hardest hit will be those accustomed to high interchange fees such as the UK, Ireland, Germany, Spain, Portugal, and several Central and Eastern European countries.

In general, the pain will be worse for credit card issuers because the MIF Regulation interchange fees are less of a change for debit cards. Nowhere will feel the pinch more strongly than the UK and Germany, where pre-regulation credit rates were at least three times higher than the new caps. Overall, EU issuers are expected to lose between €5–6 billion annually in interchange revenues.

One bright spot for card issuers is the fact that centrally-billed corporate cards are exempt from the rate caps. But corporate cards where the balance is charged to the cardholder rather than the company will be subject to the caps, inducing most issuers to either convert cardholder-liability cards into company-liability cards or introduce additional fees.

To compensate for decreased revenues, issuers are reducing rewards levels, increasing cardholder fees, simplifying product sets, reducing expenses, and considering new opportunities such as lower scheme fees through co-badging.

Caps have little impact on three-party schemes

Three-party schemes, such as Amex and Diners, do not operate with separate issuers and acquirers like other card schemes and are therefore mostly unaffected by the MIF Regulation’s rate caps. They can continue to invest the revenue from their premium fees into marketing, cardholder benefits, and other innovations.

Acquirers and PSPs benefit while facing technical and operational challenges

Acquirers and PSPs benefit from increased margins because they have no obligation to pass the savings from rate caps on to merchants. Most large merchants will be savvy enough to obtain cost savings immediately but most small and medium-sized merchants will not in the near-term. Yet over time this benefit for acquirers and PSPs will erode as competition forces them to pass more of the cost savings to merchants. PSPs and acquirers can expect a two to three year window of increased margins, as illustrated below.

While on balance the MIF Regulation rate caps are positive for acquirers and PSPs, there are downsides. First, the structure of the interchange caps does not benefit issuers from more secure processing such as 3-D Secure, which creates a disincentive for merchants to invest in supporting security measures. Second, the pricing transparency requirements and customer choice at the point of sale create technical and operational demands that will challenge acquirers and PSPs. Ensuring that processing systems and statements support interchange++ pricing and the need to obtain merchant consent in writing before bundling pricing may be significant hurdles, especially for smaller acquirers with older, inflexible systems. These challenges are made more painful by the fact that the pricing transparency measures are unlikely to affect acquirers and PSPs materially because many merchants prefer the simplicity of bundled pricing.

Merchants will see cost savings coming soon

Merchants are the clear beneficiaries of the interchange caps. Large merchants and savvy SMEs will wring cost reductions from their payment providers immediately. The lower fees will be reflected in bundled rates as well, but such a shift will take months or even years.

Making the most of the new environment

As the ground shifts for all actors—issuers, acquirers, payment service providers, and merchants—those that take action sooner rather than later will be better positioned to benefit, both immediately and over the long-term.

The new white paper, “Driving Change with PSD2 and the MIF Regulation: Creating Opportunities in Europe,” provides a fuller description of the MIF Regulation and PSD2, their impact upon the payments industry, and guidance for a proactive response. Read it today.