a guide to fednow

The FedNow® Service, Explained: Here’s What You Need To Know

Insights into the new Federal Reserve Bank’s instant payments service

On This Page

Key Takeaways

- The FedNow Service is an instant payments infrastructure developed and operated by the U.S. Federal Reserve Bank, offering 24/7/365 real-time gross settlement to eligible depository institutions nationwide.

- Unlike legacy systems such as ACH and Fedwire, FedNow settles payments individually, immediately, and irrevocably, at any hour, on any day of the year.

- Participation is flexible. Institutions can configure any combination of send, receive, liquidity management, and settlement capabilities to suit their business needs and risk appetite.

- FedNow is built on the ISO 20022 messaging standard and is use-case agnostic, supporting a wide and growing range of payment types.

- FedNow complements rather than replaces existing payment rails, adding a centrally operated instant payments option alongside ACH, Fedwire, and private-sector networks.

What is the FedNow Service?

The FedNow Service is an instant payments service being developed by the United States Federal Reserve Bank (Fed). The FedNow Service, or FedNow, offers uninterrupted 24/7/365 processing and features integrated clearing functionality, enabling financial institutions to deliver end-to-end instant payment services to their customers.

What are instant payments?

Instant payments refer to any account-to-account funds transfer that allows for the immediate availability of funds to the beneficiary of the transaction. Though timings may differ from one scheme to the next, payments are often completed in a matter of seconds. For these reasons, instant payments are also commonly referred to as immediate payments or real-time payments. Some of the benefits of instant payments are their irrevocability, their ability to generate rich data and their 24/7/365 availability.

How does the FedNow Service differ from Fedwire?

The Fedwire Funds Service is a real-time gross settlement system designed to support electronic funds transfer between banks, businesses and government agencies. Fedwire is capable of instantaneously posting and settling payments; however, Fedwire has limited availability and can only process payments on designated business days and during business hours. By comparison, the FedNow Service is not subject to nightly, weekend or holiday restrictions; it is available all hours of the day, every day of the year.

It is important to note, though, that FedNow transactions are limited to a maximum value; FedWire does not impose a limit, though one may be set by your bank.

What is the availability of the FedNow Service?

The FedNow Service operates 24/7/365, which means users can initiate, process, and settle payments at any time of the day, on any day of the year, including nights, weekends, and federal holidays. This always-on availability is one of the most significant distinctions between FedNow and legacy payment systems such as Fedwire and ACH, which are subject to processing windows and cutoff times. For financial institutions and their customers, this means time-sensitive payments, such as payroll disbursements, emergency transfers, or supplier payments, are no longer constrained by business hours or calendar dates.

Who is eligible to participate in the FedNow Service?

According to official Fed documentation:1

“As with all Federal Reserve Bank services, the FedNow Service is available to depository institutions eligible to hold accounts at the Reserve Banks under applicable federal statutes and Federal Reserve rules, policies, and procedures. Participants are able to designate a service provider or agent to submit or receive payment instructions on their behalf. Participants are also able to settle payments in the account of a correspondent, if they choose to do so. Merchants, consumers, or non-bank payment service providers can access the service through depository institutions as they do today with other payment systems.”

What features are included in the FedNow Service?

In addition to around-the-clock availability and integrated clearing functionality, the FedNow Service is designed to be flexible, allowing financial institutions to configure their participation around their own business objectives and risk appetite. Institutions can generally enable any combination of the following participation types,2 and can adjust their configuration at any time through the FedNow interface via FedLine Solutions:

Send and Receive

Institutions that choose to send and receive will have the ability to send, receive and return customer payments; to send and receive credit transfers from other financial institutions to support instant payment liquidity needs; to send customer-initiated Requests for Payment (RfPs) and to opt to receive RfPs on behalf of customers.

Receive Only

Institutions that choose to receive only will be able to receive payments from other financial institutions to meet liquidity needs, return payments received and send — but not receive — RfPs.

Liquidity Management Transfers

Institutions that opt into liquidity management transfers will have the ability to complete high-dollar-limit credit transfers with other financial institutions at scheduled times, even when the Fedwire Funds Service is unavailable.

Settlement Services

Institutions that choose to participate in settlement services will gain support for correspondent/respondent relationships; more specifically, FedNow transactions for financial institutions that use correspondents will settle in the correspondent’s master account.

The first release of FedNow included fraud prevention tools and payments inquiry support. It also included a liquidity management tool, available to FedNow participants and their traditional liquidity providers, as well as participants in private-sector instant payment services that use a joint account at a Reserve Bank.

Why did the Federal Reserve Bank develop FedNow?

Instant payments are one of the fastest-growing forms of digital payments, with the value of transactions processed using this technology projected to grow3 289 percent between 2023 and 2030. Central banks in more than 50 countries have already implemented instant payment networks that support the immediate posting and settlement of funds.

U.S. consumers and corporations can already access instant payments via Zelle and the RTP® Network; these are both privately held systems, owned and operated by Early Warning Services, LLC and The Clearing House, respectively. The Fed first began to explore the possibility of introducing a centrally owned and operated instant payments network in 2013 and formed the Faster Payments Task Force (FPTF) in 2015 to identify opportunities to implement instant payments.

In its final report, published in 2017, the FPTF overwhelmingly ruled in favor of establishing a network and issued recommendations to support successful implementation. In 2018, the U.S. Treasury offered its official support for an instant payments network, and in 2019, the Federal Reserve Board announced that it would begin developing the FedNow Service.

Ultimately, the Fed developed FedNow to enable financial institutions of all sizes across the U.S. to provide safe and efficient instant payment services to customers.

Did FedNow replace the ACH Network?

No, the FedNow Service did not replace the Automated Clearing House Network (ACH); instead, it complements ACH services.

A bit of background: ACH is a U.S.-based electronic funds transfer network for consumers, businesses, and federal, state and local governments. It is commonly used to complete direct deposit and direct payment transactions. ACH transfers typically take anywhere from one to three business days to complete.

The National Automated Clearing House Associations, or NACHA — the organization responsible for ACH governance — introduced Same Day ACH in 2016. As its name implies, Same Day ACH posts and settles payments the same day that they’re initiated — a significant improvement, but not exactly immediate. For this reason, Same Day ACH is considered a faster payments system rather than an instant payments system.

Rather than replace ACH or Same Day ACH, the FedNow Service provides greater redundancy for payment operations, thereby preventing any potential payment network bottlenecks. In the longer term, the Fed intends to establish payments interoperability between the FedNow Service and ACH.

How does the FedNow Service work?

The FedNow Service is a real-time gross settlement system, which means each payment is processed, cleared, and settled individually and immediately, rather than being batched and settled at the end of the day (as is the case with ACH). Payments are initiated as credit transfers, meaning the sending institution pushes to the receiving institution on behalf of the customer; the payee does not pull funds from the payer’s account.

All messages transmitted across the FedNow Service conform to the ISO 20022 messaging standard, which enables rich, structured data to accompany each payment. This supports greater straight-through processing, more efficient reconciliation, and improved fraud detection.

Financial institutions connect to the FedNow Service via the Federal Reserve’s FedLine network and must maintain sufficient funds in their Federal Reserve master account — or in the master account of a designated correspondent — to cover outgoing payments. This prefunding requirement ensures that settlement is immediate and final, with no credit risk introduced to the system.

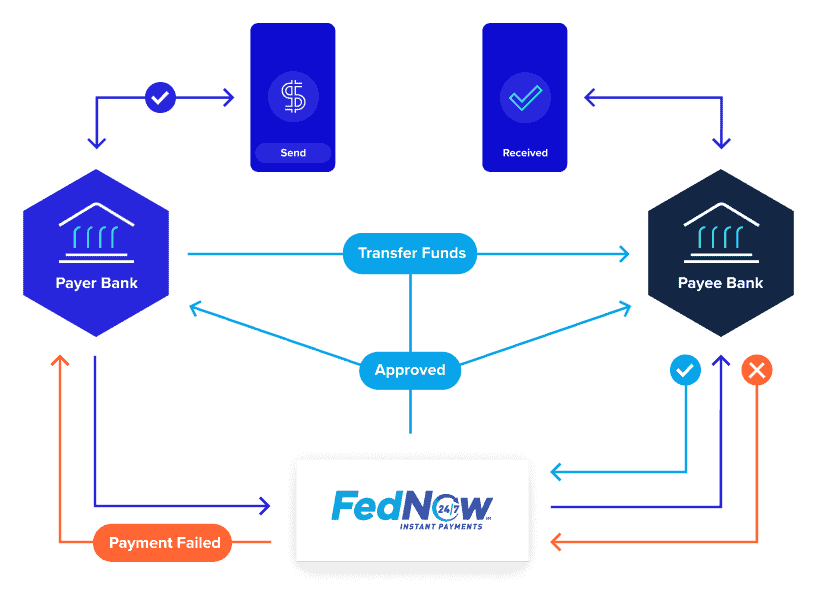

What does a FedNow payments flow look like?

A FedNow payments flow is similar to any other instant payments flow, starting with the parties involved: a payer, the payer’s financial institution, the FedNow network, a payee and the payee’s financial institution.

The general process is as follows:

- A payer initiates a payment by sending a payments message to their financial institution through an end-user interface outside of the FedNow Service.

- The payer’s financial institution receives the payments instruction and, provided the payer has sufficient funds in their account, authorizes the transaction.

- The payer’s financial institution submits a payments message to the FedNow Service.

- The FedNow Service validates the payments message and sends the contents of that message on to the payee’s financial institution for acceptance or rejection.

- The payee’s financial institution sends a response to the FedNow Service either accepting or rejecting the payments message. If the payee’s financial institution rejects the message, the FedNow Service will notify the payer’s financial institution of payments failure. If the payee’s financial institution accepts the message, the FedNow Service automatically deducts funds from the payer’s account and posts them to the payee’s account.

- The FedNow Service notifies all parties of the successful transfer of funds, and the transaction is complete.

How do financial institutions benefit from the FedNow Service?

Since its launch, the FedNow Service has been well-received4, offering tangible benefits to financial institutions and their customers. Use cases and transaction volumes continue to expand with ongoing adoption.

The FedNow Service enables financial institutions to:

- Strengthen their competitive position by meeting growing demand for instant payments. A Federal Reserve survey5 revealed that 66 percent of U.S. businesses are likely to use instant payments if their primary financial institution offers them, and those that do reported 10 percent higher satisfaction with their bank than those that do not. On the consumer side, six in 10 consumers6 consider it important for their financial institution to offer instant payments, with that figure rising to 78 percent among Gen Z respondents.

- Access instant payments infrastructure, regardless of institutional size. Unlike some payments infrastructure that has historically favored large banks, the FedNow Service was built with broad participation in mind, and the majority of institutions that currently live on the network are community banks and credit unions.

- Support a wide variety of payments and use cases. The FedNow Service does not limit the types of payments it can support, leaving product innovation to financial institutions and their partners. This approach has already yielded a diverse set of high-value applications, spanning consumer, business, and government payments alike.

- Improve customer cash flow and financial flexibility. Instant, irrevocable settlement gives recipients immediate and unconditional access to funds, removing the uncertainty that comes with batch-processed payments. For individuals, this translates to faster access to wages and reimbursements; for businesses, it supports liquidity management and strengthens supplier relationships through reliable, timely settlement.

- Access richer payment data through ISO 20022. Because FedNow is built on the ISO 20022 messaging standard, each transaction can carry significantly more structured data than legacy payment rails allow. This supports a higher degree of straight-through processing, reduces the need for manual reconciliation, and creates a foundation for more sophisticated fraud detection

- Fight back against fraud. FedNow participants have reported very low incidence of fraud on the network to date, and the Fed continues to expand its suite of risk management tools in response to industry feedback.

What was the launch date of the FedNow Service?

The FedNow Service launched in July 2023. The service went live with a founding cohort of financial institutions and has expanded steadily since, growing to more than 1,500 participating bands and credit unions across all 50 states. The Fed has described broad adoption across the industry as a gradual journey and continues to add new features and capabilities in response to growing commercial demand.

How was the FedNow Service rolled out?

The FedNow Service was rolled out in stages; the initial launch included core clearing and settlement functionality, Request for Pay capability, and tools to support reconciliation.

In preparation for its target release date, the Fed asked more than 110 organizations — including ACI Worldwide — to participate in its FedNow Pilot Program. As a program participant, ACI helped shape the FedNow Service’s features and functions, provided input into the overall user experience and ensured readiness for testing, all of which helped define the FedNow Service’s service and adoption roadmap, industry readiness approaches, and overall instant payments strategy.

What are the limitations of the FedNow Service?

While the FedNow Service offers numerous advantages over traditional payment systems, there are some limitations to be aware of:

- FedNow transactions are subject to a network-level per-transaction limit, which the Fed has the ability to adjust over time in response to market demand. Individual financial institutions may set their own limits within the bounds of the network cap based on their risk tolerances and business needs. Transactions that exceed those limits will need to be routed through an alternative channel, such as Fedwire.

- Because instant payments settle immediately and irrevocably, FedNow transactions cannot be reversed once completed. This places greater pressure on both financial institutions and their customers to verify payment details before initiating a transfer, and it makes fraud prevention a critical consideration for participants.

- Access to FedNow is limited to eligible depository institutions that have joined the service; financial institutions not yet connected to the network cannot send or receive payments through the service. While FedNow participation has grown steadily since its launch, it remains well below the total number of depository institutions in the U.S., which means network coverage is still maturing.

What was the launch date of the FedNow Service?

The FedNow Service launched in July 2023. The service went live with a founding cohort of financial institutions and has expanded steadily since, growing to more than 1,500 participating bands and credit unions across all 50 states. The Fed has described broad adoption across the industry as a gradual journey and continues to add new features and capabilities in response to growing commercial demand.

Article Sources

- Board of Governors of the Federal Reserve System, “FedNow® Service: Frequently Asked Questions, https://www.federalreserve.gov/paymentsystems/fednow-additional-questions-and-answers.htm.” ↩︎

- The Federal Reserve, “FedNow Readiness Guide, https://explore.fednow.org/resources/readiness-guide-participation-types.pdf.” ↩︎

- Statista, “Instant/real-time payments – statistics & facts, https://www.statista.com/topics/11304/instant-or-real-time-payments/.” ↩︎

- Federal Reserve Bank Services, “FedNow Service: Two Years of Growth and Innovation, https://www.frbservices.org/news/fed360/issues/071625/fednow-service-two-years-growth-innovation.” ↩︎

- The Federal Reserve, “New survey: Innovative use cases drive businesses to instant payments, https://www.frbservices.org/news/fed360/issues/050125/industry-perspective-faster-payments-survey-business.” ↩︎

- The Federal Reserve, “Financial Institutions Can Use Instant Payments to Attract Customers, Improve Satisfaction and Lower Risk of Attrition, https://fedpaymentsimprovement.org/news/blog/financial-institutions-can-use-instant-payments-to-attract-customers-improve-satisfaction-and-lower-risk-of-attrition/.” ↩︎

Get Ready for FedNow Service Instant Payments

Jumpstart your real-time payments revolution by getting access to the connections you need to seamlessly integrate into the FedNow Service network